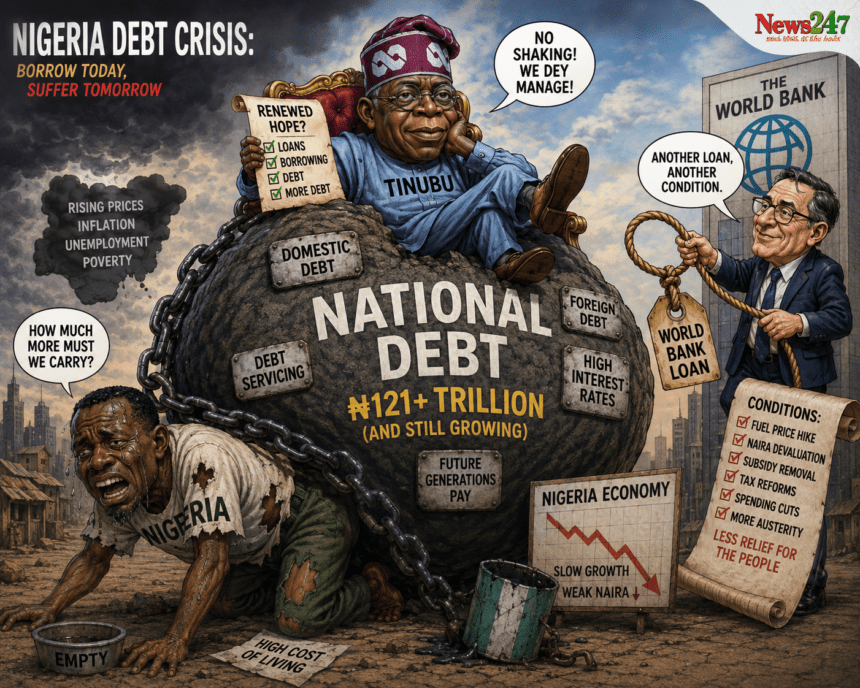

According to the Debt Management Office, the country’s total public debt as of December 31, 2025 stood at $110.97 billion or N159.28 trillion. But, President Bola Tinubu, in the Africa Forward Summit in Nairobi, has just revealed that the country will be paying about N11.6 trillion to service and pay that debt in 2026 alone — almost half of the projected revenue of the country for the year. It is over twice as high as the $5.15 billion of debt-service costs in 2025. But, even with this jaw-dropping amount of outstanding debt, the Federal Government is in advanced discussions with the World Bank for a new $1.25 billion loan called the Nigeria Actions for Investment and Jobs Acceleration programme, which will be reviewed by the World Bank board on June 26, 2026.

These are not abstract numbers! They are the arithmetic of a country which is in a borrowing binge while it is quietly binging its future.

Nigerians have no choice but to be ironic about the president’s address in Nairobi. President Tinubu, representing the people of Nigeria before the international community, reiterated the criticism of the international financial system as regressive against the people of Africa. He was concise and articulate. He said that if every one of those dollars that we pay in punitive interest rates is not invested in our steel sector, textile mills, agro-processing plants or our digital industries, then that is a dollar we lost. We agree entirely. But Nigerians should also hear the other side of that sentence forcefully at home, from the same government that is moaning about its debt load in Nairobi, which is making the gravitation of more debt to the load even faster.

- THE ILLUSION OF MARKET RECOVERY: Why Paper Appreciation of the Naira Cannot Cure Underlying Structural Liquidity Defects

- THE PRICE OF PARALYSIS: Why the Oyo Education Shutdown Exposes the Total Failure of Local Security

- THE SUPERFICIAL SHIELD: Why Airport Thermal Scanners Will Not Save Nigeria from the New Ebola Threat

To examine the human cost of this debt burden means it is useful to observe what it actually entails. The combined sum of N68.3 trillion in the appropriation bill for 2026 demonstrates that N15.52 trillion is allocated to debt servicing alone, which is more than even allocation for education (N3.52 trillion), health (N2.48 trillion) and infrastructure (N3.56 trillion). That is, Nigeria will be paying over 4 times more for education budget and over 6 times more for health budget on loan — many of which were obtained ostensibly for education and health budget. In March 2026, civic organisation BudgIT cautioned that the country was not in the immediate position of being able to come out of a range of 50-60 percent debt servicing ratio in revenue. The government will get back N100 per N70 borrowed.

The situation is not good governance. This is no less than a conservative fiscal drift.

I know the difficult budget constraints that the Tinubu administration inherited and have made some structural changes like the elimination of petrol subsidy, consolidation of foreign exchange banking recapitalisation and the removal of Nigeria from the Financial Action Task Force (FATF) grey list. Such are not insignificant actions. External reserves have increased to $45.5 billion and some deceleration has been seen in the debt/GDP ratio. While not large in sum, they are not to be taken lightly. The gains from macro are of little benefit to the 139 million Nigerians because from a recent evaluation by the World Bank of this latest loan application, 63 percent of Nigerians are still in poverty as of 2025. Citizens’ trust is being eroded and investors’ trust is growing.

In addition, in-depth examination of the nature of Nigeria’s borrowing should be considered. As has been pointed out, in recent years a greater proportion of new loans has been devoted to “recurring expenditures and debt payments” rather than to “transformative assets.” The borrowing of money is not investment if it is used for the repayment of existing debts, but is instead “treading water” at progressively greater cost to the country. Under the current administration’s debt stock has increased by N71.82 trillion since June 2023, which is equivalent to 45 per cent of the total debt stock. The Nigerian Economic Summit Group has strongly cautioned that Nigeria has not yet made a true trajectory towards debt sustainability and the country is still operating in high risk fiscal environment. It is not possible for the assessment to be ignored.

In addition to the political timing of the proposed $1.25 billion World Bank loan is the troubling political timing. It will be on the board on June 26, 2026, six months and twenty-one days before the presidential election Jan. 16, 2027. It is documented by the World Bank itself that “political and governance risks are high prior to the 2027 elections, and pressures are likely to stall or roll back sensitive reforms. It’s fair to consider this an investment for the long run or to think about adding liquidity ahead of an election cycle. The Nigerians who emerged this week to condemn the World Bank for giving Nigeria fresh loans are not economic illiterates. They are citizens who have been having their dollars borrowed in their names for minimal gains in their lives.

We don’t want you to paralyze the economy! Nigeria requires capital. The infrastructure shortfall is a fact of life. Investment for power, roads and agriculture and investment for digital connectivity are needed. But borrowing must be disciplined, purposeful and transparent — not reflexive. The proof of a record of the work done by previous loans must be present and public before any new loans can be contracted. The Debt Management Office shall make the conditions, disbursement rates and impacts of all facilities of the current administration easily accessible and easily published. Put an end to National Assembly approving loans as an administrative formality – their mandate is to authorise these loans. We can’t afford to take the easy way out at this moment and simply rubberstamp.

We are calling on the Tinubu administration to do the following: First, present Nigerians with a comprehensive debt sustainability plan – a plan that is truthful in terms of timelines, targets and trade-offs – a plan that does not mislead these Nigerians by telling them they are under debt when they are not. Second, ensure that all new loans are applied to capital expenditure projects that can be clearly and tangibly linked to spending, and not to recurrent spending. Third, diversify revenue forcefully. The challenge of Nigeria’s fiscal situation has been the lack of good domestic revenue generation practices rather than being a debt problem, as many analysts have been claiming. Tax reform won’t fix the N30 trillion shortfall in revenue, it’s up to the real economy. Fourth, there should be no temptation to the government to resort to borrowing as a political lubricant. Political spending of today’s borrowed money will make up the debt of tomorrow’s generation.

Nigeria is not a poor country. It’s a country that has a long and painful history of bad management of its resources. The President is correct on saying that the international financial system is an enemy to African countries. Nairobi speech no matter how righteous does not bring down a debt-service bill. What makes it to go down is orderly borrowing, profitable investment and the kind of effort toward domestic revenue making that makes the nation less dependent upon the creditors in the first place.

Do not allow the payment of the debt to take place today and leave money to borrow tomorrow to pay for it. This already bloated bill is steadily continuing to expand and it will be ordinary Nigerians who will bear the burden.

Discover more from News247 Nigeria

Subscribe to get the latest posts sent to your email.